Navigating the complexities of retirement planning can be daunting, especially for high-income earners who find themselves above the income limits for direct Roth IRA contributions.

Enter the Backdoor Roth IRA—a strategic workaround that allows individuals to maximize their retirement savings by indirectly contributing to a Roth IRA.

This comprehensive guide demystifies the Backdoor Roth IRA process, outlining who should consider it, the pros and cons, tax implications, step-by-step instructions, and how to avoid common pitfalls. Understanding the Backdoor Roth IRA can significantly enhance your retirement strategy, whether you're a seasoned investor or just embarking on your financial journey.

A Bit of History: The Roth IRA

The Roth IRA is named after Senator William Roth, a committed Delaware politician who was pivotal in creating this retirement account. Thanks to his legislative efforts, individuals can now contribute after-tax dollars to a Roth IRA and enjoy tax-free withdrawals in retirement. In essence, the "Roth" in Roth IRA honors Senator Roth for establishing a valuable tool that empowers people to save for a comfortable and tax-efficient retirement.

Strategic Process: The Backdoor Roth IRA involves contributing to a Traditional IRA and then converting those funds to a Roth IRA.

Eligibility: Best suited for high-income earners who exceed direct Roth IRA contribution limits.

Tax Implications: Critical to understand the Pro-Rata Rule and accurately report conversions to avoid tax pitfalls.

Avoiding Mistakes: Timely conversions, proper reporting, and managing IRA balances are essential to fully harnessing the benefits.

Consult Professionals: Given the complexity, seeking advice from financial advisors or tax professionals can ensure compliance and optimize outcomes.

Integrating the Backdoor Roth IRA into your retirement strategy can enhance your financial security, achieve greater tax diversification, and ensure a comfortable and prosperous retirement. Stay informed, plan diligently, and leverage this strategy to its fullest potential.

A Backdoor Roth IRA allows individuals to contribute to a Roth IRA even if their income exceeds the standard eligibility limits. This is achieved by converting a traditional IRA into a Roth IRA, a process sanctioned by the IRS as a legitimate workaround to the income restrictions on direct Roth IRA contributions.

A Backdoor Roth IRA is not a standalone financial product but a strategic process that enables high-income earners to contribute to a Roth IRA despite exceeding the income limits set for direct contributions. This method involves two primary steps:

Contribute to a Traditional IRA: Make a non-deductible contribution to a Traditional IRA.

Convert to a Roth IRA: Convert the funds from the Traditional IRA to a Roth IRA.

By understanding the regulations governing both Traditional and Roth IRAs, individuals can effectively leverage the Backdoor Roth IRA to enhance their retirement savings.

High-income earners often face restrictions on contributing directly to a Roth IRA due to income caps. The Backdoor Roth IRA provides a legal avenue to bypass these limitations, allowing for tax-free growth and withdrawals in retirement—a key advantage of Roth IRAs.

Not everyone needs to use a Backdoor Roth IRA. It is specifically beneficial for individuals whose income exceeds the thresholds for direct Roth IRA contributions. Here’s a detailed breakdown:

Income Limits: For 2024, the ability to contribute directly to a Roth IRA phases out at a Modified Adjusted Gross Income (MAGI) of $161,000 for single filers and $240,000 for married couples filing jointly.

Contribution Limits: For 2024, individuals can contribute up to $7,000 annually to an IRA, or $8,000 if they are 50 or older. The IRS has kept these limits unchanged for 2025.

Roth IRA Contribution Limits (Tax Year 2025) | ||||

Single Filers (MAGI) | Married Filing Jointly (MAGI) | Married Filing Separately (MAGI) | Maximum Contribution for individuals under age 50 | Maximum Contribution for individuals age 50 and older |

under $150,00 | under $236,000 | $0 | $7,000 | $8,000 |

$151,500 | $237,000 | $1,000 | $6,300 | $7,200 |

$153,000 | $238,000 | $2,000 | $5,600 | $6,400 |

$154,500 | $239,000 | $3,000 | $4,900 | $5,600 |

$156,000 | $240,000 | $4,000 | $4,200 | $4,800 |

$157,500 | $241,000 | $5,000 | $3,500 | $4,000 |

$159,000 | $242,000 | $6,000 | $2,800 | $3,200 |

$160,500 | $243,000 | $7,000 | $2,100 | $2,400 |

$162,000 | $244,000 | $8,000 | $1,400 | $1,600 |

$163,500 | $245,000 | $9,000 | $700 | $800 |

$165,000 & over | $246,000 & over | $10,000 & over | $0 | $0 |

High-Income Earners: Those earning above the Roth IRA income limits but below the thresholds for a Mega Backdoor Roth IRA.

Married Couples: Especially those where at least one spouse has a high income, making it challenging to contribute directly to a Roth IRA.

Low-Income Earners: If your income allows for direct Roth IRA contributions, it’s more straightforward to contribute directly.

Those Without Traditional IRAs: If you don’t have a Traditional IRA and prefer not to open one solely for this purpose, the Backdoor Roth may not be suitable.

Timing plays a crucial role in maximizing the benefits of a Backdoor Roth IRA. Here’s what you need to consider:

Annual Contribution Window: Contributions for a given tax year can be made from January 1 of that year until April 15 of the following year. For instance, 2024 contributions can be made up until April 15, 2025.

Flexibility in Conversion: Unlike contributions, Roth conversions have no deadline within the tax year. You can convert funds at any time, whether immediately after the contribution or years later.

Best Practices: To maximize tax-free growth, it’s advisable to convert funds soon after making the Traditional IRA contribution. This minimizes the window during which the funds could earn taxable income, simplifying tax reporting and reducing potential complications.

Market Conditions: Converting when the market is down can result in a lower taxable amount, as the value of the assets being converted is reduced.

Tax Bracket Management: Converting in a year when your income is lower than usual can minimize the tax impact of the conversion.

Like any financial strategy, the Backdoor Roth IRA has advantages and disadvantages. Understanding these can help you make an informed decision.

Access to Roth IRA Benefits: Tax-free growth and tax-free withdrawals in retirement.

No Income Limits for Conversions: Unlike direct contributions, conversions do not have income restrictions.

Tax Diversification: Balances tax-deferred accounts with tax-free accounts, offering flexibility in retirement.

Estate Planning Advantages: Roth IRAs can be inherited tax-free, providing benefits to heirs.

No RMDs: Roth IRAs do not require minimum distributions during the owner’s lifetime, allowing for continued growth.

Complexity: The process involves multiple steps and careful adherence to IRS rules.

Pro-Rata Rule: Existing Traditional, SEP, or SIMPLE IRAs can complicate the tax implications of conversions.

Potential for Mistakes: Incorrectly executing the steps can lead to unintended tax consequences.

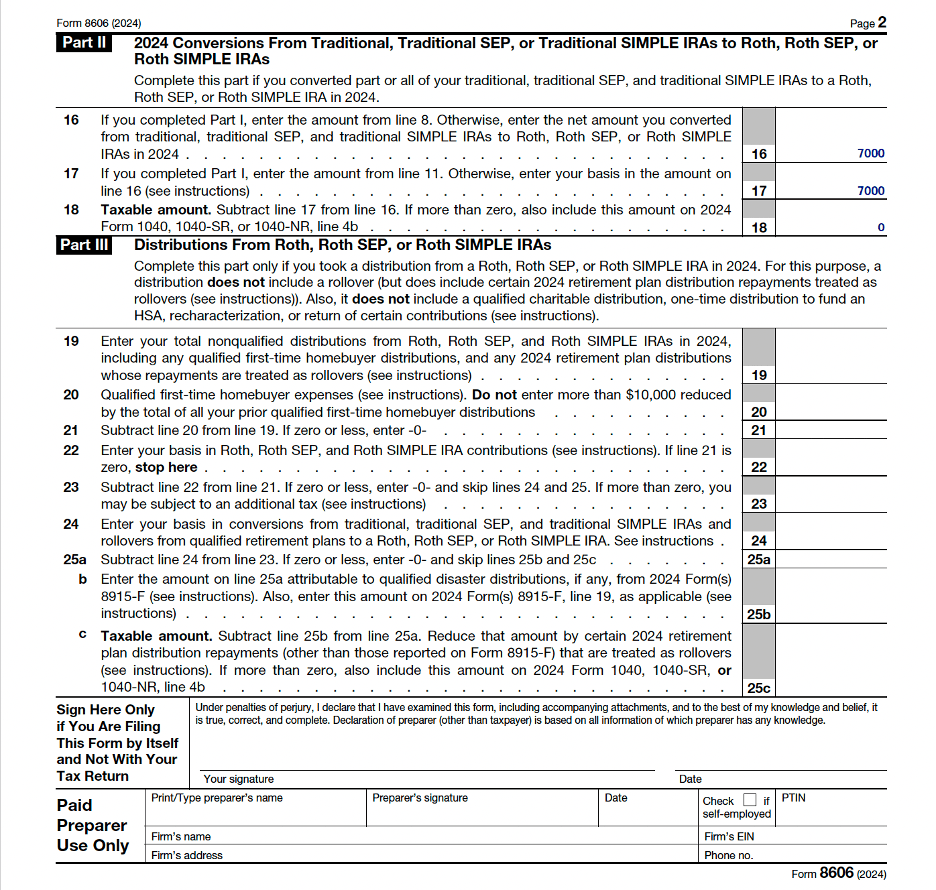

Form 8606 : is critical for reporting non-deductible contributions and conversions related to your Roth account.

Tax Liability on Conversions: If not executed properly, conversions can result in unexpected taxable income.

While the Backdoor Roth IRA offers significant tax advantages, it requires meticulous planning and execution to avoid unexpected income tax consequences. High-income earners who can navigate the complexities effectively may find it a worthwhile strategy to enhance their retirement savings.

Understanding the tax implications is essential to avoid costly mistakes and optimize the benefits of a Backdoor Roth IRA. Here’s a deep dive into the key tax considerations:

The Pro-Rata Rule is a critical IRS regulation that affects the taxability of Roth conversions. It stipulates that the taxable portion of a Roth conversion is proportional to the pre-tax and post-tax assets across all your Traditional, SEP, and SIMPLE IRAs.

Calculation Basis: The IRS looks at the total balance of all Traditional, SEP, and SIMPLE IRAs you own.

Taxable Amount: The taxable portion of your conversion is determined by the ratio of pre-tax contributions to the total IRA balance.

Example 1: Suppose you have a Traditional IRA with $150,000 in pre-tax contributions and $50,000 in post-tax contributions. If you convert $8,000 to a Roth IRA, 75% ($6,000) of the conversion will be taxable, and 25% ($2,000) will be tax-free.

Details | Amount | Taxable Percentage |

Total IRA Funds (pre-tax + post-tax) | $200,000 |

|

After-Tax Contributions | $50,000 | 25% |

Pre-Tax Contributions | $150,000 | 75% |

Amount to be Converted | $8,000 |

|

Taxable Portion (75% of $8,000) |

| $6,000 |

Example 2: Suppose you have a Traditional IRA with $100,000 in pre-tax contributions. If you convert $7,000 to a Roth IRA, 100% ($7,000) of the conversion will be taxable.

A properly executed Backdoor Roth IRA conversion can result in zero tax liability on the converted amount if:

The contribution to the Traditional IRA was non-deductible (post-tax).

The conversion is done before any significant earnings accrue in the Traditional IRA.

However, if the Pro-Rata Rule applies due to existing pre-tax IRA balances, a portion of the conversion may be taxable.

Form 8606: Required to report non-deductible contributions to Traditional IRAs and conversions to Roth IRAs.

Form 1099-R: Received from the IRA custodian, indicating the amount converted.

Form 5498: Reports IRA contributions and rollovers.

Accurate reporting is crucial to ensure compliance and avoid penalties. Mistakes in reporting can lead to double taxation or IRS penalties.

Executing a Backdoor Roth IRA involves a series of deliberate steps. This section provides a detailed walkthrough to help you navigate the process smoothly.

Action: Make a non-deductible contribution to a Traditional IRA.

Contribution Limits: The limit for 2024 is $7,000, or $8,000 if you are 50 or older.

Non-Deductible Contribution: Ensure that your contribution is non-deductible by not claiming a deduction on your taxes. This is crucial to avoid double taxation.

ExampleIf you contribute $7,000 to a Traditional IRA, this amount is considered after-tax money, assuming you cannot deduct the contribution due to high income-tax liabilities.

Action: Keep your Traditional IRA funds in a low-risk investment, such as cash or a money market fund, to minimize gains or losses between contribution and conversion.

Why: Minimizing earnings ensures that the conversion process is straightforward and reduces the taxable amount.

Best Practice: Convert the funds as soon as possible after the contribution to prevent significant growth.

Action: Transfer the funds from your Traditional IRA to a Roth IRA.

Timing: Ideally, perform the conversion shortly after contributing to avoid taxable earnings.

Process:

Log into your IRA provider’s platform.

Initiate a Roth conversion, selecting the Traditional IRA as the source and the Roth IRA as the destination.

Complete the conversion, acknowledging any prompts about the tax implications.

Example: Convert the entire $7,000 from your Traditional IRA to a Roth IRA immediately after the contribution.

Action: Allocate the converted funds into your preferred investment vehicles within the Roth IRA.

Options: Stocks, bonds, mutual funds, ETFs, or other investment instruments based on your financial goals and risk tolerance.

Strategy: Align your investments with your overall retirement strategy, considering factors like diversification and growth potential.

Action: Manage your IRA balances to comply with the Pro-Rata Rule.

How: Avoid having pre-tax funds in any Traditional, SEP, or SIMPLE IRAs when performing the conversion.

Solution: Roll over pre-tax IRA funds into a 401(k) or other employer-sponsored retirement plans to exclude them from the Pro-Rata calculation.

ExampleIf you have an existing Traditional IRA with pre-tax contributions, transfer those funds into your employer’s 401(k) to isolate your non-deductible contributions for the Backdoor Roth IRA process and facilitate a future contribution to a Roth IRA.

Action: Accurately report the Backdoor Roth IRA contribution and conversion on your tax forms.

Form 8606: Complete Part I for non-deductible contributions and Part II for conversions.

Instructions:

Part I: Report the non-deductible contribution to the Traditional IRA.

Part II: Report the Roth conversion, ensuring that the taxable amount is correctly calculated based on the Pro-Rata Rule.

Deadline: File Form 8606 by the tax filing deadline (typically April 15 of the following year).

Example: If you contributed $7,000 to a Traditional IRA and converted the entire amount to a Roth IRA, Form 8606 should reflect the non-deductible contribution and the subsequent conversion, showing a $0 taxable amount if done correctly.

Despite its advantages, the Backdoor Roth IRA process is susceptible to errors that can negate its benefits. Here’s how to avoid and rectify common mistakes.

Failing to Convert Quickly: Allowing funds to earn taxable income before conversion complicates the process.

Ignoring the Pro-Rata Rule: Existing pre-tax IRA balances can trigger taxable conversions.

Incorrect Reporting on Tax Forms: Errors on Form 8606 can result in double taxation or penalties.

Contributing Directly to a Roth IRA: High-income earners inadvertently contributing directly can lead to excess contributions.

Overlooking Spousal IRAs: Married couples might miss opportunities to maximize their Roth contributions through spousal IRAs.

Prompt Conversion: Convert funds immediately after making the Traditional IRA contribution to minimize taxable earnings.

Isolate Non-Deductible Contributions: Transfer pre-tax IRA funds to a 401(k) or other employer-sponsored plans to comply with the Pro-Rata Rule.

Accurate Tax Reporting is essential for maintaining compliance with Form 8606 in relation to your Roth account.: Carefully fill out Form 8606 or seek professional assistance to ensure correct reporting.

Understand Contribution Limits: Ensure you are not exceeding the allowable contribution limits for both Traditional and Roth IRAs.

Utilize Spousal IRAs: For married couples, contribute to both spouses' IRAs to maximize the Backdoor Roth strategy.

Recharacterization: If you accidentally contribute directly to a Roth IRA, you can recharacterize the contribution to a Traditional IRA by contacting your IRA provider before the tax filing deadline.

Amending Tax ReturnsIf you discover errors after filing, you may need to file an amended return (Form 1040X) to correct Form 8606 and ensure accurate tax reporting for your Roth account.

Professional Assistance: Engage a tax professional or financial advisor to help rectify complex mistakes and ensure compliance.

Contributions to a Backdoor Roth IRA can be made up until the tax filing deadline of the following year, providing flexibility in the timing of contributions and conversions. Here’s how to handle late contributions effectively.

Timeframe: Contributions for a specific tax year can be made from January 1 of that year until April 15 of the next year.

Example: For the 2024 tax year, contributions can be made until April 15, 2025.

When making a contribution after the end of the calendar year but within the contribution window:

Separate Reporting: Report the contribution for the prior year and the conversion for the current year.

Form 8606Ensure that the non-deductible contribution is reported on the prior year’s Form 8606 and the conversion on the current year’s Form 8606 to comply with tax law.

Documentation: Maintain clear records of the contribution and conversion dates to avoid confusion during tax filing.

Action: Contribute $7,000 to a Traditional IRA in March 2024 for the 2023 tax year.

Conversion: Convert the $7,000 to a Roth IRA in May 2024, reported on the 2024 tax return.

Form 8606:

2023: Report the $7,000 non-deductible contribution.

2024: Report the $7,000 Roth conversion.

Maximized Growth: Early contributions allow more time for investments to grow tax-free within the Roth IRA.

Simplified Reporting: Keeping contributions and conversions within the same year minimizes paperwork and reduces the potential for errors.

Recharacterization is the process of reversing a Roth IRA contribution or conversion back to a Traditional IRA. This can be necessary if you exceed income limits or make other errors in the Backdoor Roth IRA process.

Exceeding Income Limits for contributions to a Roth IRA can affect your eligibility for a Backdoor Roth conversion.: If you inadvertently contribute directly to a Roth IRA despite high income, recharacterization can correct the excess contribution.

Incorrect Conversion: If you convert funds at an inopportune time, resulting in higher taxable income, recharacterization can mitigate the tax impact.

Change in Financial Circumstances: Alterations in your financial situation may necessitate recharacterizing contributions for better tax efficiency.

Contact Your IRA Provider: Notify them of your intent to recharacterize the Roth IRA contribution to a Traditional IRA.

Complete the Transfer: Your IRA provider will facilitate the transfer of the contribution plus any earnings or minus any losses to a Traditional IRA.

Document the Recharacterization: Ensure you receive confirmation of the recharacterization and keep all related documents for tax reporting.

Report on Tax Forms:

Form 8606: Report the recharacterized contribution as a Traditional IRA contribution.

Form 1040: Include a statement explaining the recharacterization if required.

Deadline: Recharacterizations must be completed by the tax filing deadline (typically April 15) of the year the contribution was made.

Separate from Conversions: Since 2018, recharacterizing Roth conversions is no longer permitted; only contributions can be recharacterized.

Tax Implications: Any earnings on the recharacterized contribution are taxable in the year of conversion.

Scenario: You contribute $7,000 directly to a Roth IRA in 2024, but your MAGI exceeds the allowable limit.

Action: Recharacterize the $7,000 to a Traditional IRA by April 15, 2025.

Tax Reporting:

Form 8606: Report the Traditional IRA contribution.

Form 1040: Attach a statement detailing the recharacterization.

Avoid Penalties: Correcting excess contributions prevents IRS penalties for overcontribution.

Maintain Tax Efficiency: Ensures your retirement savings strategy remains aligned with your financial situation and tax planning.

A Backdoor Roth IRA is a method that allows high-income earners to contribute to a Roth IRA indirectly by first making a non-deductible contribution to a Traditional IRA and then converting it to a Roth IRA.

Individuals whose income exceeds the Roth IRA contribution limits but who still have eligibility to contribute to a Traditional IRA can utilize the Backdoor Roth IRA strategy.

While there are no income limits for converting a Traditional IRA to a Roth IRA, there are income limits for making direct Roth IRA contributions. The Backdoor Roth IRA circumvents these limits by using conversions.

Due to the Pro-Rata Rule, the taxable portion of the conversion depends on the proportion of pre-tax and post-tax contributions in all your Traditional, SEP, and SIMPLE IRAs. Proper execution of the Backdoor Roth conversion can minimize or eliminate tax liability.

Yes, you can perform a Backdoor Roth IRA conversion annually, provided you adhere to IRS rules and contribution limits.

The Pro-Rata Rule dictates that the taxable portion of a Roth conversion is proportional to the total balance of all your Traditional, SEP, and SIMPLE IRAs. This rule prevents taxpayers from isolating non-deductible contributions for tax-free conversions.

Report the non-deductible Traditional IRA contribution on Form 8606, and the Roth conversion on the same form. Ensure accurate completion to avoid double taxation or penalties.

Risks include misreporting on tax forms, triggering taxable conversions due to the Pro-Rata Rule, and the potential for legislative changes that could affect the strategy's viability.

No, it is primarily beneficial for high-income earners who are ineligible for direct Roth IRA contributions. Others may benefit more from direct contributions or different retirement savings strategies.

The Backdoor Roth IRA is a powerful tool for high-income earners seeking to maximize their retirement savings through tax-advantaged accounts. By understanding the mechanics, adhering to IRS regulations, and meticulously executing each step, individuals can effectively bypass income limitations and enjoy the long-term benefits of Roth IRAs.

By adhering to the guidelines and strategies outlined in this guide, you can confidently navigate the Backdoor Roth IRA process, ensuring your retirement savings are optimized for growth and tax efficiency.